Background and Scale of the Crisis

On 28 February 2026 Iranian forces began Operation Epic Fury, launching drone and missile strikes against Israeli and U.S. assets. In response, the U.S. and Israel attacked Iranian targets, prompting Iran's Revolutionary Guard Corps to declare that the Strait of Hormuz — a 30-mile-wide waterway through which roughly 20% of globally traded oil and almost the same share of liquefied natural gas normally pass — was unsafe for commercial shipping.

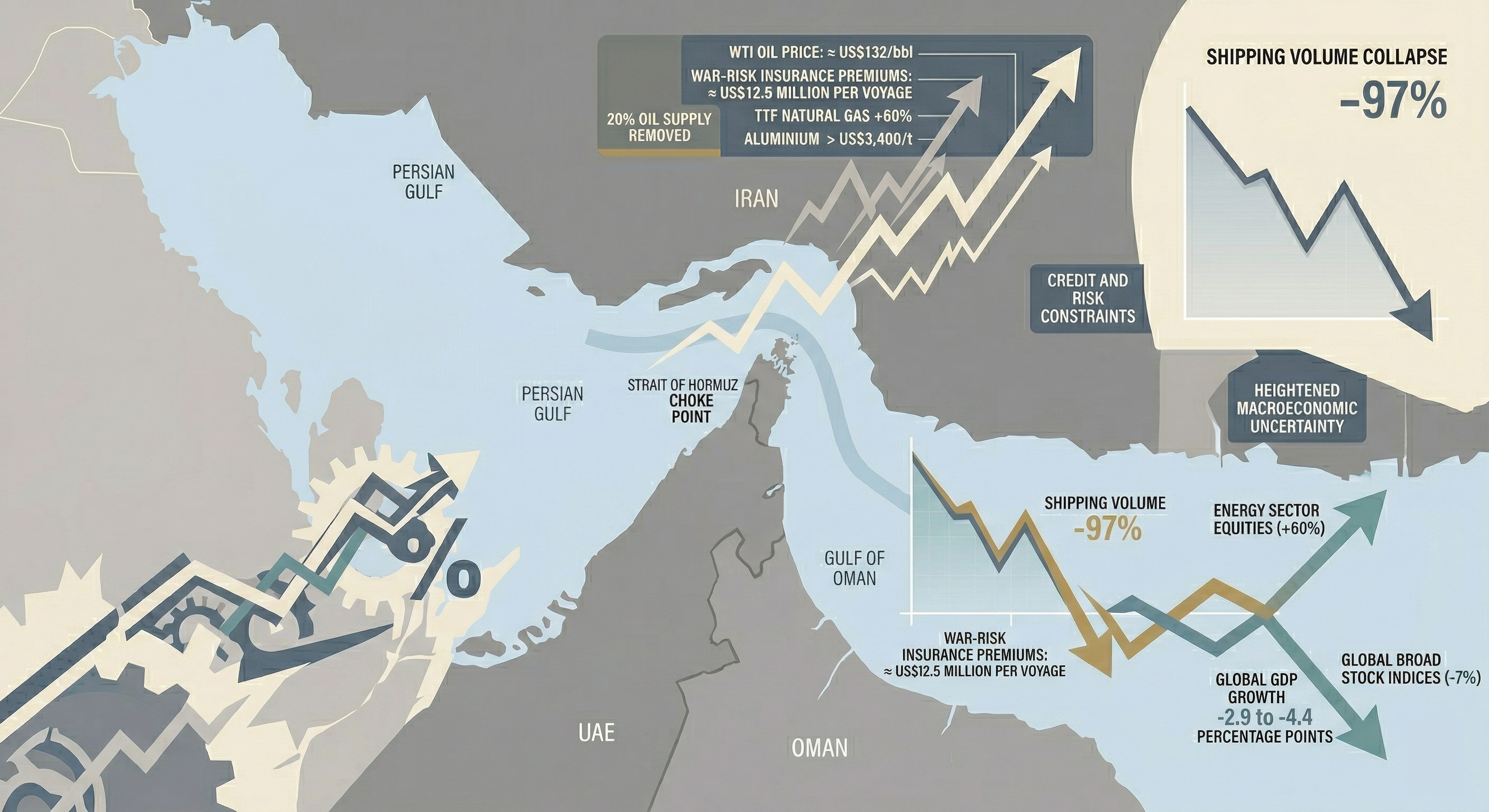

Insurers withdrew coverage and maritime tracking firms reported that ship traffic fell by 70% within a day. By early March the strait was effectively closed to vessels from the U.S. and Israel, causing tankers and container ships to anchor outside the Gulf and divert around Africa's Cape of Good Hope, adding 2–3 weeks to voyages and raising costs by over US$250,000 per trip.

The immediate effect was a jump in energy prices: Brent crude rose over 15% in the first trading session after the closure and climbed above US$100 a barrel in the weeks that followed. War-risk insurance premiums for ships transiting the Gulf rose from 0.02%–0.05% of a vessel's value to 0.5%–1%, implying additional costs of US$600,000–1.2 million on a US$120 million tanker. The conflict also disrupted one-third of the world's fertiliser trade, 30% of jet-fuel supply, and critical container hubs such as Dubai's Jebel Ali port.

A complete closure removes about 20 million barrels per day (≈20% of global oil supply), and pipeline alternatives can move only 3.5–5.5 million bpd. Emergency reserves could cushion the shock for 1–3 months but sustained closures would push oil prices toward US$200 per barrel and shrink world GDP growth below 2%. The current analysis builds on that baseline and avoids repeating those arguments.

Short-term Windfalls

- Higher revenues for U.S. energy producers. As global prices surged, U.S. shale and Gulf-coast producers enjoyed windfall profits from selling oil and liquefied natural gas. Although only about 8% of U.S. crude imports came from the Persian Gulf, global prices feed into domestic fuel costs; analysts at Rice University's Baker Institute and Energy Intelligence observed that energy companies' profits rose while consumers paid more at the pump. Conservative commentators framed the crisis as a chance to "bet on the world after the conflict" and predicted that regional states would eventually fund a permanent security arrangement to police the strait.

- Leverage in negotiations. Pro-Trump outlets reported that President Donald Trump weighed seizing Iran's Kharg Island, which handles about 90% of Iran's crude exports, to force Tehran to reopen the strait. Supportive lawmakers backed decisive action, while retired military leaders warned that the cost and duration would be significant. By projecting readiness to use force, the administration can pressure Iran and signal resolve to allies without immediately deploying ground troops.

- Domestic political messaging. Pro-Trump media portrayed the closure as exposing international "free-riders" who rely on U.S. security. Discussions suggested that after the war the strait would be policed by a coalition of regional states paying for stability, and a "short-term pain for long-term stability" narrative emerged. The messaging seeks to frame the crisis as an opportunity to cripple Iran's revenue and force a favourable settlement while strengthening the image of American resolve.

Structural Benefits and the U.S.–China Rivalry

- Test of hegemonic credibility. Analysts at the Middle-East think-tank EISMENA argue that the closure is a "stress test" of the post-1945 liberal economic order. They note that U.S. leadership is unusual because the hegemon itself caused the breakdown of freedom of navigation. Every week the U.S. fails to reopen the strait erodes its credibility as provider of global public goods and allows challengers to argue that American hegemony no longer guarantees stability.

- China's vulnerabilities and resilience. Roughly 40% of China's crude imports and 30% of its LNG imports transit the Hormuz strait, and alternative pipelines through Saudi Arabia and the UAE can carry <40% of Gulf export traffic. Yet Chinese vulnerability is more nuanced. War on the Rocks observes that China is 85% energy self-sufficient and that oil forms only ≈18% of its total energy consumption because coal and renewables dominate. China's strategic reserves cover 3–4 months of imports and are supplemented by diversified land routes and discounted Iranian crude.

- China's strategic opportunities. Beijing has chosen neutrality, publicly avoiding taking sides while positioning itself as a responsible mediator. Chinese commentators believe China has "very little to lose by staying quiet and a lot to gain by being seen as a neutral party." U.S. military engagement in the Middle East could divert attention from the Indo-Pacific, allowing China to expand influence and promote its Global Security, Governance, Civilisation, and Development initiatives.

When Do Benefits Turn into Costs?

The U.S. gains from higher energy exports and strategic leverage only if the disruption remains short-lived. Several analyses pinpoint a tipping point beyond which the closure becomes economically and politically damaging for Washington:

- Duration of the shock. The LSE's Khezri stresses that emergency reserves and pipeline rerouting can bridge 1–3 months; beyond that period, the global supply shortfall becomes unsustainable and could trigger inflation and growth shocks. Market strategist David Fyfe outlines scenarios: a one-month closure is manageable; a three-month interruption significantly increases inflation and delays interest-rate cuts; a six-month closure forces rate hikes and drags global GDP growth below 2%, essentially stalling the world economy.

- Inflation and consumer backlash. U.S. gasoline prices rose by about 56 cents per gallon following the closure. War-risk premiums boosted shipping costs by 200–300%, costs that "will soon be felt at gas pumps and supermarkets." With Republican mid-term electoral pressure, Trump will avoid allowing high energy prices to persist.

- Risk of stagflation. EISMENA's analysis warns that the combination of supply-driven inflation and demand contraction — a "toxic combo" — could trap central banks. Prolonged disruption raises the prospect of stagflation, forcing policymakers to choose between tolerating higher inflation or inducing a recession.

In summary, the U.S. enjoys leverage and energy-export gains if it can restore passage quickly. If the closure lasts beyond two or three months or if oil prices approach US$150 per barrel, the benefits vanish and the crisis turns into a political liability and potential global recession.

Global Recession Scenarios

Inflation and Energy Prices

- Rapid price escalation. Energy adviser Bob McNally (Rapidan Energy) told CNBC that a long disruption would be an "assured hit" to the world economy. Wood Mackenzie analysts compared the situation to the 1970s oil crisis and argued that oil prices would need to reach US$200 to trigger a comparable global downturn. The IEA chief Fatih Birol cautioned that the Iran oil crisis is the worst energy shock ever recorded and said world leaders are not ready for its consequences.

- Supply-side inflation beyond oil. The strait closure halts a third of global fertiliser shipments and threatens food security in South Asia. It also disrupts helium and aluminium supplies and worsens the semiconductor shortage. Such bottlenecks echo the COVID-19 supply-chain crisis but differ by being geographically concentrated and energy-centric.

- War-risk insurance and freight costs. War-risk premiums have increased 200–300%, costing US$600,000–1.2 million per voyage. Rerouting around Africa adds 2–3 weeks and raises shipping costs by ≈US$250,000 per voyage. These extra costs feed into consumer prices, particularly for Asian economies that depend heavily on imports.

Supply Chain Disruptions and Other Indicators

- Energy rationing and industrial impact. The closure directly affects industries reliant on Gulf LNG and oil. The crisis threatens fertiliser production and technologies such as semiconductors, while shortages of fertiliser, aluminium and helium could curb crop yields and industrial output. Qatar's suspension of LNG production at Ras Laffan in anticipation of further strikes tightens European gas markets.

- Financial markets and interest rates. A sustained closure keeping Brent around US$100 per barrel would shave 0.5 percentage points off global growth and add 1 percentage point to inflation. Central banks might delay rate cuts or even raise rates to counter rising prices; David Fyfe warns that a six-month closure could force rate hikes and push global growth below 2%, effectively a recession.

- Stockpiles and resilience. Countries with large strategic reserves fare better. China's reserves cover 3–4 months and China has diversified pipelines, while the U.S. can tap its Strategic Petroleum Reserve but has already drawn it down after the 2022 price shock. Japan and South Korea's limited reserves mean they may face rationing within weeks.

Scenario Analysis

| Closure duration | Oil price & inflation | Growth / recession risk | Supply-chain impacts |

|---|---|---|---|

| <1 month quick reopening |

Brent spikes to $100–120, then falls as strait reopens; inflation rises modestly. OPEC's spare capacity and U.S. reserve releases cushion the shock. | Global GDP dips slightly (<0.5 ppts); recession unlikely. Markets treat the event as a temporary shock. | Minimal; shipping schedules normalize quickly. |

| 1–3 months prolonged partial closure |

Oil averages $120–150; supply-side inflation broadens to fertiliser, metals and semiconductors. War-risk premiums persist. | Central banks delay rate cuts; global growth slows markedly. Risk of recession rises in Asia and Europe; U.S. consumers feel pain despite energy export gains. | Significant rerouting strains shipping; Asian economies face energy rationing; fertiliser shortages threaten crop yields. |

| >3 months extended closure |

Oil could exceed $150; such levels constitute an "assured" global recession. Stagflation emerges as inflation accelerates while growth contracts. | Global recession becomes likely; growth <2% and possible rate hikes. U.S. political pressure mounts to reopen the strait. | Severe supply-chain breakdowns; food and fuel shortages in South Asia; global manufacturing disruptions. |

Comparative Gains and Losses for the United States and China

The Hormuz crisis interacts with U.S.–China rivalry in complex ways. The table below summarises potential advantages and vulnerabilities for each side. While both countries can extract short-term benefits, those gains erode rapidly as the conflict drags on.

| Factor | United States | China |

|---|---|---|

| Energy revenue & inflation | Beneficiary of high oil prices: U.S. shale and LNG producers enjoy windfall profits, and the government can use strategic reserves to manage domestic supply. Benefits fade if the closure persists beyond 1–3 months. | Vulnerable to supply shocks because ~40% of crude imports and 30% of LNG imports transit Hormuz. Nevertheless, Middle Eastern oil makes up only one-third of refining needs, and China is 85% energy self-sufficient. |

| Military leverage | Opportunity to demonstrate naval dominance and pressure Iran, projecting resolve to allies. Risk of being drawn into prolonged conflict and diverting resources from the Indo-Pacific. | Opportunity to observe U.S. operations, portray itself as neutral and responsible. Prolonged conflict could accelerate China's energy diversification and alignment with Russia. |

| Diplomatic narrative | Gains if able to build a multinational coalition to secure the strait, reinforcing U.S. leadership. Risks eroding credibility if it cannot reopen the strait quickly. | Gains by advocating non-interference and negotiation. China "has very little to lose by staying quiet and a lot to gain by being seen as a neutral party." |

| Domestic politics | Conservative commentators tout decisive action. Yet rising petrol prices and inflation risk voter backlash and complicate efforts to cut interest rates. | Domestic price controls and state-owned energy firms insulate Chinese consumers. Extended disruption could hurt manufacturing, but the crisis provides impetus to accelerate renewables. |

In summary, the United States gains in the very short term from energy exports and geopolitical leverage, but these benefits dissipate if the closure lasts beyond a few months. China is vulnerable to supply disruptions yet possesses buffers — diversified energy sources, strategic reserves and state controls — that limit immediate damage while offering the chance to accrue diplomatic capital by advocating neutrality.

Comparing Hormuz to the COVID-19 Supply-Chain Shock

- Nature of the shock. COVID-19 produced a demand shock as lockdowns halted consumption, whereas the Hormuz closure is primarily a supply shock that constrains energy and shipping capacity. Both crises expose vulnerabilities in global just-in-time logistics.

- Inflation dynamics. During the pandemic, inflation initially fell as energy prices collapsed; later supply bottlenecks pushed prices higher. By contrast, the Hormuz closure caused immediate energy-driven inflation. Sustained closure could trigger stagflation — a risk largely avoided in the early pandemic because monetary and fiscal stimulus could support demand.

- Policy responses. Governments responded to COVID-19 with massive fiscal stimulus and central bank easing. In a Hormuz-induced energy shock, policymakers face a trade-off: easing monetary policy fuels inflation, while tightening to tame prices deepens the downturn.

- Supply chain reconfiguration. COVID-19 accelerated diversification away from concentrated production hubs. The Hormuz crisis similarly underscores the need to diversify energy routes. China viewed strait closures as likely battlefields and therefore invested in pipelines and reserves.

- Geopolitical consequences. The pandemic did not fundamentally alter the balance of power between the U.S. and China. The Hormuz closure, by contrast, directly implicates U.S. naval dominance and tests hegemonic stability. Each week of closure undermines American credibility and opens space for China and Russia to benefit.